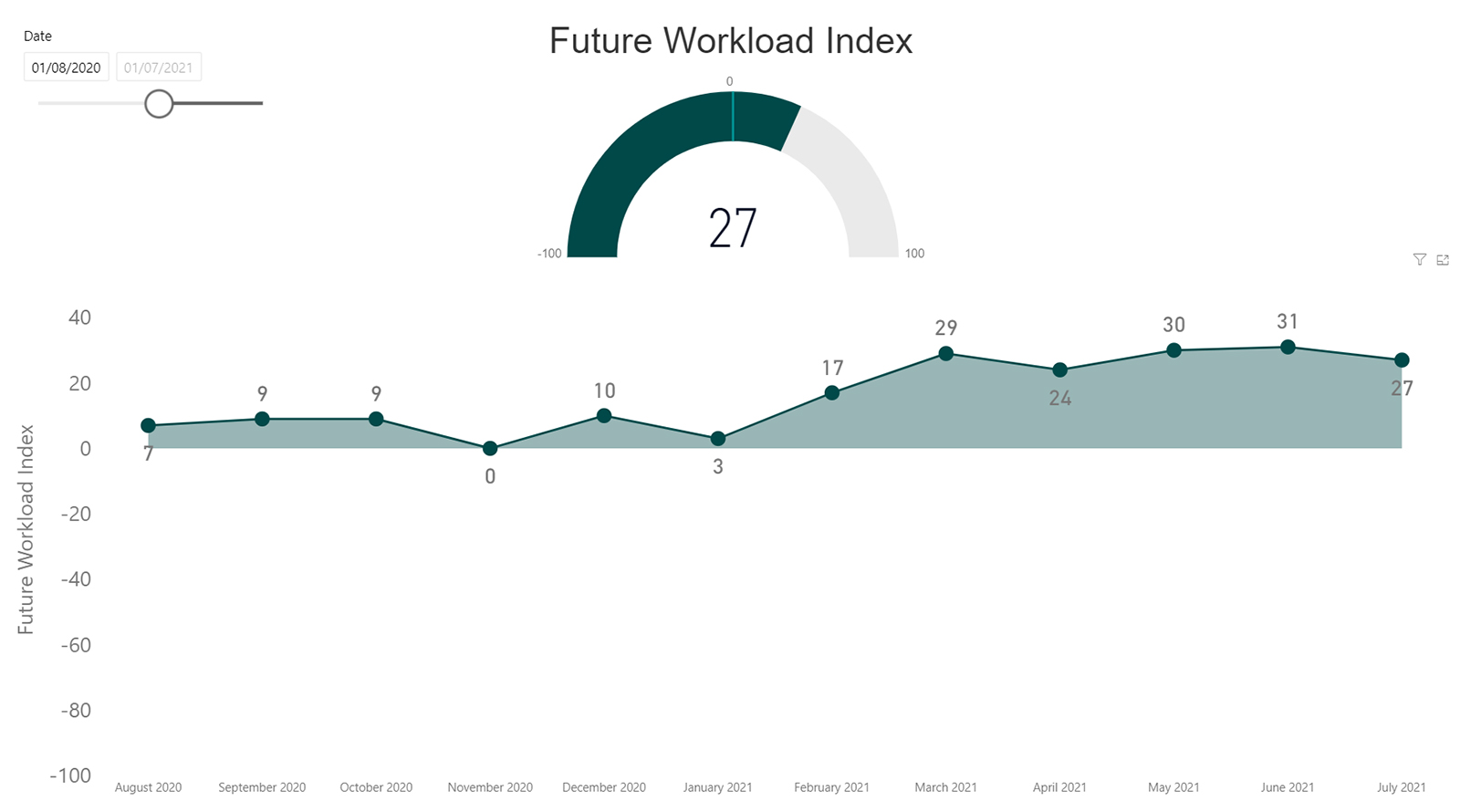

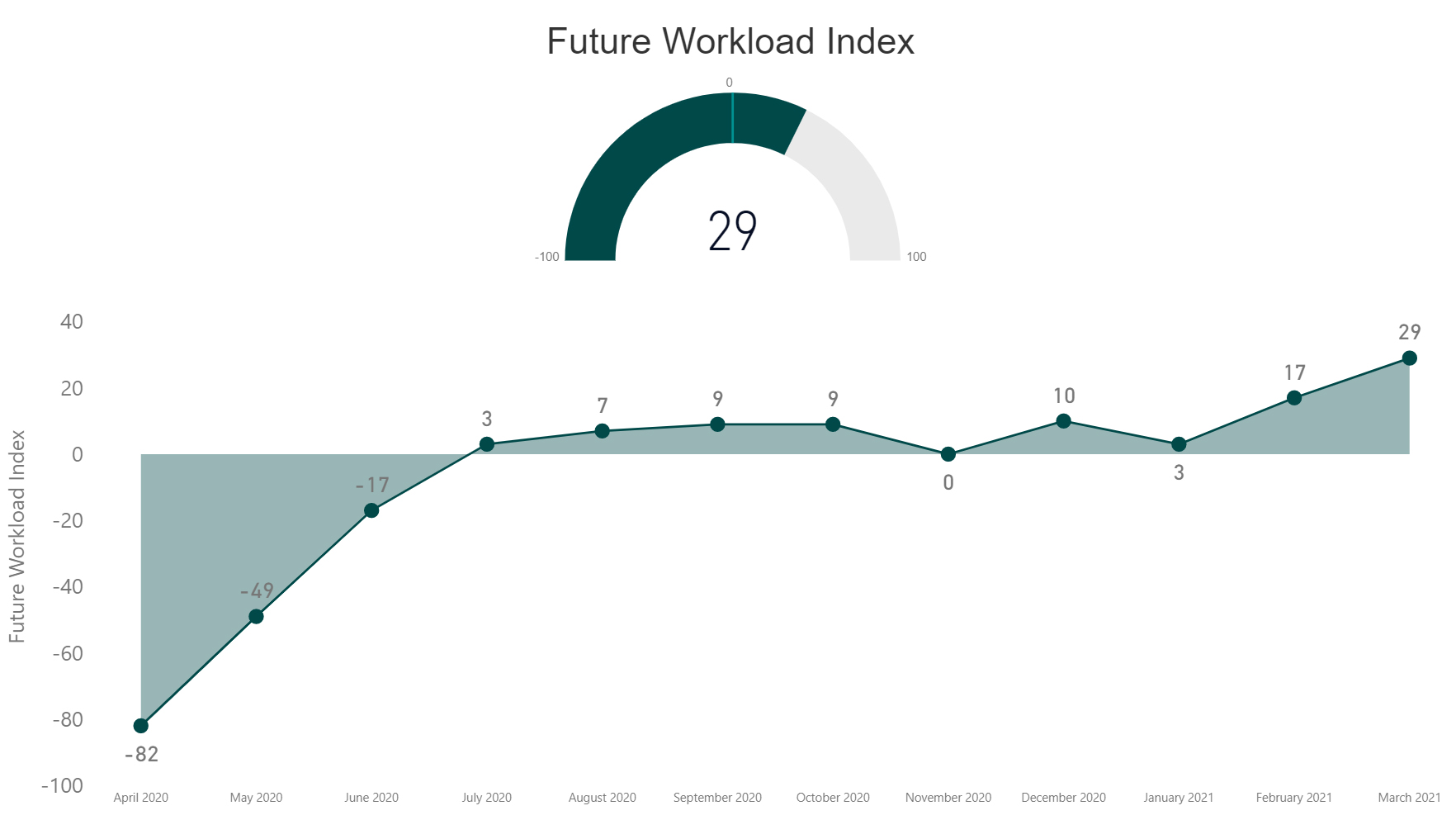

In March the RIBA Future Trends Workload Index rose by 12 points to a balance figure of +29. This is the highest Workload Index balance figure since May 2016. In the last 12 months, the index has risen by an unprecedented 111 points.

All regions are becoming more positive about future work. London is the largest architecture market in the UK and, for the first time since February 2020, practices there are anticipating increasing workloads in the coming months, with a balance figure of +18 an increase of 21 balance points from -3 in February.

Forty per cent of practices expect workloads to grow in the coming three months, whilst just under half (49%) expect them to remain the same. The percentage expecting workloads to decrease has fallen again and now stands at 11% (compared to 84% a year ago). Optimism about future workloads continues to be driven by the private housing sector, although the outlook for all sectors is improved from last month.

Practices of all sizes are expecting workloads to increase, with larger practices the most optimistic. March feels like a significant turning point.

The outlook of Small practices (1 – 10 staff) again rose strongly. In March small practices posted a future workload balance figure of +27 up fourteen points from February’s figure of +13. Confidence among Large and Medium sized practices (11 – 50 and 51+ staff) remains strong, with an overall balance score of +42, up 13 points on last month’s figure of +29.

March sees the South of England grow in confidence, with a balance figure of +32 this month, up from zero last. The Midlands & East Anglia has risen further into positive territory up fourteen points from last month to +20. Wales & the West posted a balance figure of +33 in March, the tenth consecutive month of a positive outlook. The most positive region this month is the North of England, with a balance figure of +47. Here only two per cent of practices expect workloads to fall, and almost a half (49%) expect them to grow.

Among the four different work sectors, private housing remains by far the strongest. However, all sectors are again up on last month, and no sector is negative. The private housing sector rose by a further 7 points to +36, a balance score that is higher than at any point since June 2015. The commercial sector returned to positive territory for the first time since the pandemic onset with a balance score of +7. Both the public sector and community sectors eased out of negative territory this month, but only just with both posting a zero balance figures.

In terms of staffing:

- The RIBA Future Trends Staffing Index increased by 3 points to +7 this month.

- 7% of practices expect to employ fewer permanent staff in the coming three months, while 14% expect to employ more. A clear majority (79%) of practices expect staffing levels to be constant over the coming three months.

- Medium and large-sized practices (11+ staff) continue to be most likely to recruit permanent staff in the coming three months, with both groups posting strongly positive figures.

- On balance, small practices (1 – 10 staff) expect staffing levels to grow somewhat, with a balance figure of +6 (up from +1), though 80% of small practices anticipate staffing levels to stay the same.

- The Temporary Staffing Index returned a balance figure of +5 (up from +1 in February).

- London remains least optimistic with a zero balance figure in March (though this is up from -8 in February). Eleven per cent of London practices expect to employ more permanent staff over the coming months with the same proportion expecting to employ fewer.

- The South of England (+4) and the Midlands & East Anglia (+2) are cautiously optimistic about upcoming recruitment.

- In line with workload expectations, the North of England (+13) and Wales & The West (+18) are the areas in which practices are most likely to expect growing numbers of permanent staff.

- Personal underemployment remained at 20% in March, and staffing levels remain at 96% of a year ago.

- Overall, since the onset of the pandemic, redundancies remain at 3% of staff. Seven per cent of staff remain on furlough. Eighteen per cent of staff are working fewer hours.

RIBA Head of Economic Research and Analysis, Adrian Malleson, said: “With the vaccine programme underway, and workload prospects improving across sectors, regions and practice sizes, March’s Future Trends data shows a profession firmly optimistic about future work.

“Personal underemployment has dropped from a high of 42% to 20%. Practices are more confident about their longer-term prospects, with 13% expecting increased profitability over the next year, and 29% expecting it to hold steady. However, the extremely positive rise in confidence does not mean that the challenges practices face have evaporated. Four per cent of practices think they are unlikely to remain viable over the next 12 months. Forty-three per cent, after an already extremely difficult period, expect profitability to decrease over the coming year.

“The commentary received in March continues to describe a housing sector performing strongly, particularly smaller-scale domestic work. Some practices report that there is more work available than they can take on.

“However, practices also mention that such work may be of comparatively low-value, and subject to intense fee competition. Longer-term, the recovery in private housing needs to be matched by growth in the public, commercial and community sectors.

“Nevertheless, March’s data confirms a remarkable restoration of confidence among practices during an unprecedented 12 months.

“We continue to be on hand, providing support and resources to our members as they navigate these challenging times.”