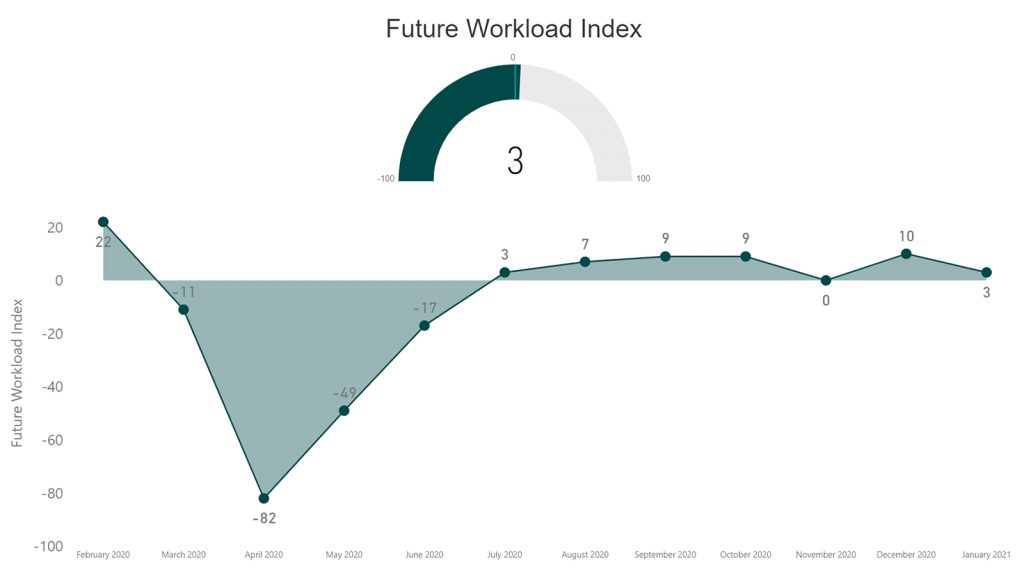

In January 2021 the RIBA Future Trends Workload Index remained positive (at +3) despite the turbulence of Brexit and a third national lockdown. Whilst 25% of practices expected workloads to decrease in the coming three months, 28% forecasted an increase. Just over half (51%) expected workloads to hold steady.

The South of England was the only region to post a negative workload balance figure this month, a fall of 10 points (to -2), although optimism also decreased sharply in the North of England (falling from +29 in December to 0). London posted a positive workload balance (+1) for the first time since February 2020. Other regions – the Midlands, East Anglia, Wales and the West remain in positive territory.

Among the four work sectors, the private housing sector was the only one to remain positive, at + 9. Having posted positive figures in December, the public and commercial sectors fell back to negative territory in January, posting -4 and -18 respectively, suggesting an expectation of falling workloads. The community sector continues to stall, falling to a balance figure of -15 in January, down from -8 in December.

Large and medium sized practices (11 – 50 and 51+ staff) remain confident; 53% expect workloads to increase, and 13% foresee a decrease (overall balance score of +39). Small practices (1 – 10 staff) however fell back into negative territory in January, posting a workload balance figure of -2, down from +4 in December.

With the UK and EU’s new trading agreement in place, the survey for the first time monitored the impact of Brexit on the attitudes of architects. Overall, the new agreement is perceived to have a negative impact on the profession; 15% more architects expect it to lead to a decrease in workload than an increase. Architects indicated they expect key areas to be detrimentally affected by the new agreement: 41% stated this to be the case regarding availability of skilled on-site staff, 54% regarding recruiting/retaining architects from outside the UK and 63% regarding the availability of building materials.

In terms of staffing:

- The RIBA Future Trends Staffing Index rose again in January (+4, from +2 in December).

- In the next three months 83% of practices expect staffing levels to remain the same, 7% expected to employ fewer permanent staff, and 10% expect to employ more.

- Medium and large-sized practices (11+ staff) continue to be those most likely to recruit permanent staff in the coming three months, with both posting strongly positive index figures. Smaller practices are more likely to expect staffing levels to hold steady, having posted a January Staffing Index figure of zero.

- The Temporary Staffing Index returned a balance figure of zero in January, suggesting the market for temporary staff will remain as is.

- London remains the region least likely to anticipate increased staffing levels in the next three months – returning a negative balance figure of –4. The South of England is also cautious – returning a balance figure of -6. Recruitment is more likely in the North of England (+14) and the Midlands & East Anglia (+8).

- Personal underemployment stands at 22%, a slight increase on last month’s figure, but within historical norms, and significantly below the high of 42% in the first lock-down.

- Staffing levels are 96% of a year ago. Overall, redundancies stand at 3% of staff. Seven per cent of staff remain on furlough.

RIBA Head of Economic Research and Analysis, Adrian Malleson, said: “It’s promising that the profession has overall maintained a positive outlook. However, with a decrease from +10 in December to +3 in January, it’s clear that the ongoing uncertainties presented by both Brexit and the third national lockdown are having an impact on confidence.

“Disparities persist across regions, practice sizes and notably sectors. That only the housing sector returned positive figures, clearly indicates the limited commitment of resources to construction, from both businesses and government.

“Whilst there are some promising signs, for example London reporting its first positive workload balance for 10 months, this increase is marginal (+1), and must be tempered by the fact that the commercial sector, so important to the profession in this region, remains fragile.

“Sustained growth of the profession, particularly in the centres of large cities, will rely on a broad-based recovery that encompasses not only the housing sector, but also the public, commercial and community sectors. This recovery is unlikely to happen whilst we remain in lock-down but can be spurred and accelerated by timely government stimulus and investment.

“We continue to be on hand, providing support and resources to our members as they navigate these challenging times.”