In September 2020 the RIBA Future Workload Index rose slightly again to +9, with 31% of practices expecting a workload increase in the coming three months. 22% are expecting a decrease, and 47% are expecting workloads to remain the same.

The anticipated growth in architects’ workload continues to be driven by optimism about private housing, by smaller practices, and by practices working outside London and the South. For larger practices, and for those in London and the South, there is more pessimism about future workloads.

58% of practices overall expect profits to fall over the next twelve months (down from 65% in August), and 6% expect that fall to threaten practice viability.

Regionally, the Midlands & East Anglia were positive about their future workload for the first time in six months, with an increase to +10 in September, up from -9 in August. Wales & the West is currently the most optimistic area; it returned a balance figure of +40 in September, up ten points from August. The North of England also remains positive about workload (at +16), though down six points from August.

Confidence is lower in London and the South. The South of England slipped back into negative territory in September, posting a balance figure of -2. London has not posted a positive balance figure since February; in September the balance figure is -12, down 3 points from the previous month. 12% of London practices also reported concerns about their long-term viability, a slight fall from last month’s figure of 14 %.

Small practices (1 – 10 staff) remained the most optimistic, with a workload figure of +10, up two points from August, while large and medium-sized practices (11 – 50 and 51+ staff) slipped back further in confidence, to -9 in September, compared to zero in August, and +13 in July.

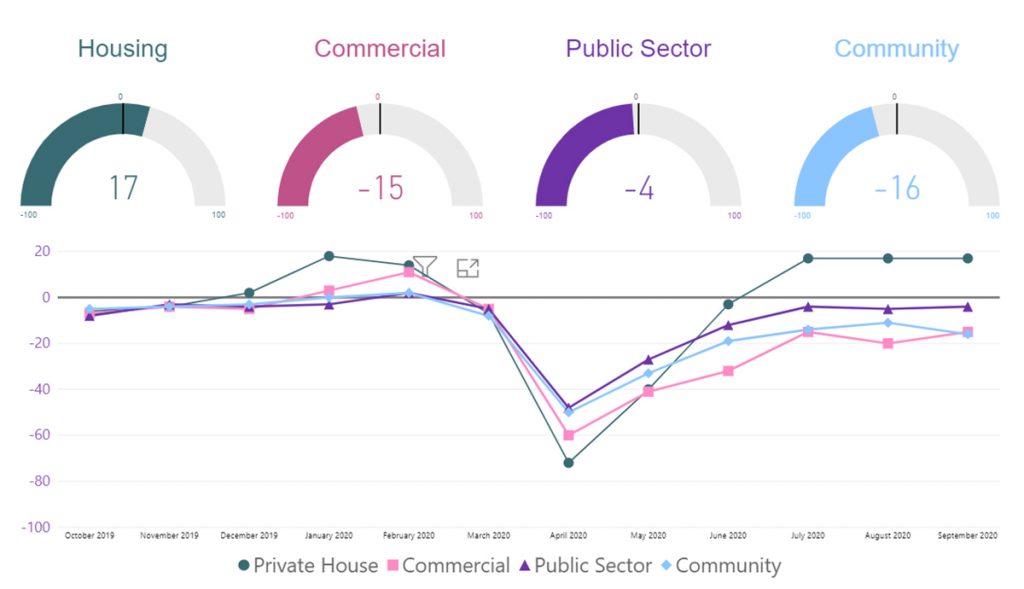

Among the four different work sectors, private housing continued to be the only area anticipating growth – returning a balance figure of +17, the same as the previous two months. The commercial sector rose five points to -15, the public sector rose by one point to -5 and the community sector fell five points to -11.

In terms of staffing:

- September has seen an increase from 22% to 48% of medium and large practices expecting a reduction in permanent staffing levels in the next three months.

- 76% of practices overall expect permanent staffing levels to remain consistent.

- 15% expect to see a decrease in the number of permanent staff over the next three months (down from 4% from August).

- 8% expect permanent staffing levels to increase.

- In London, the Staffing Index, at -19, is the lowest in the country. 22% of practices in the region expect to be employing fewer permanent staff in the next three months.

- Wales & the West is the only area where permanent staffing levels are expected to increase, recording a balance figure of +9.

- In September, the anticipated demand for temporary staff remains subdued with a balance figure of zero, up slightly on August’s figure of -2.

- Personal underemployment reported has fallen from 32% in August to 25% in September

- The average percentage of furloughed staff fell slightly from 10% to 9%.

- 19% of staff are working fewer hours than they were pre-Covid, with those in London still most likely to be working fewer hours.

- Across England, an average of 3% of staff have been made redundant (up from 2% last month). Staffing levels are 94% of what they were 12 months ago.

RIBA Head of Economic Research and Analysis, Adrian Malleson, said: “These results highlight a notable decline in confidence for medium and large practices, with almost half now expecting to reduce permanent staff in the next three months – more than double compared to four weeks ago. London and the South in particular are expecting a difficult time ahead, with a significant number of practices continuing to question long-term viability.

“Practices also describe increasing competition for work which is exerting downward pressure on fees and is clearly unsustainable. That said, many practices are remaining positive, with practices outside London and the South more likely to report an increase in enquiries this month. Maintaining and improving this outlook will depend on how the economy is supported over the coming months. Members will continue to receive dedicated support, resources and advocacy from the RIBA, which is arguably more important now than ever.”